Valuation is an essential topic in real estate. There are many methods for this, used by market players such as real estate agents, surveyors, developers, investors, or notaries.

The purpose of this article is to explain how to value a property in real estate using the right method for your specific situation.

Valuation by replacement cost

Replacement cost is certainly the easiest to understand and apply. It is the method used by insurers to determine the amount to be compensated. It simply involves considering that an identical property will be rebuilt on the land (already acquired) and applying a depreciation factor based on the condition of the property (often a simple coefficient relative to the year of construction).

It is therefore necessary to distinguish between two replacement values:

- Replacement cost new : this is simply the value of a similar property to be built

- Replacement cost: this is the replacement cost new to which a depreciation factor (discount) is applied

| Replacement cost new price | 300.000€ |

| Depreciation coefficient (depending on the age of the building) | 0,7 |

| Replacement value | 300,000 x 0.7 = €210,000 |

According to the calculation above, a replacement value does not allow the building to be rebuilt identically since a reducing factor has been applied to the replacement cost new.

Note that for the replacement-cost value to be comparable to the other methods, you must add the value of the land (which is automatically included in the other methods).

Why add the value of the land? When you rebuild a building, the cost of the land does not disappear, since the land remains unchanged. The reconstruction cost only takes into account what it costs to rebuild the building, but the land also has a value, often significant in certain areas (for example in city centers or in sought-after locations).

Thus, if the replacement value of the building after depreciation is €210,000, you must add the value of the land to obtain a complete estimate. For example, if the land is worth €100,000, the total value of the property would be €210,000 (building) + €100,000 (land), i.e. €310,000.

Valuation by income capitalization

In the capitalization approach, value is linked to the property’s rental income. The equation for the value of the property is as follows:

Current value = Net operating income / Capitalization rate

The capitalization rate is determined based on observation of the local market and the segment considered. Indeed, the capitalization rate depends on:

- Location: the capitalization rate is lower in good locations. The underlying logic is that an investor accepts a slightly lower rent if the location is very good. Conversely, to attract an investor to a smaller city, the capitalization rate will need to be high (proportional to the yield).

- The segment: the capitalization rate in commercial real estate and retail is higher than in residential, notably to cover the risk of vacancy.

To take an example, an investment property whose annual net operating income is 700,000 euros and whose capitalization rate is 6% would be worth €11.7M.

The advantage of this method is that it takes into account the property’s actual yield. It tends to overestimate properties with a good yield (e.g., a student housing building) and underestimate properties with a poor yield (e.g., a single-family house).

Are you looking to determine rental income or a capitalization rate in a concrete case? Check out our article how to value a property by capitalization to find out how to obtain this information directly in our analysis tool Market Explorer.

Valuation by comparison

Also called the “comparables method,” it is probably the most used and the most intuitive method since it simply involves comparing a property with similar properties nearby. These properties will then be compared, taking into account their similarities and their differences.

Indeed, two properties will never be perfectly identical. One of them may have been partially renovated while the other has not; one of them may also have a veranda, a swimming pool, or another element increasing its market value.

You will first need to obtain comparables (via a listing site or a comparables tool) in order to list them in an Excel table with the essential characteristics.

For a residential property, here is the main information to collect:

- The sale date or listing date

- The price

- The number of bedrooms

- The living area (as stated on the PEB energy certificate for example)

- The condition of the property

- Energy performance

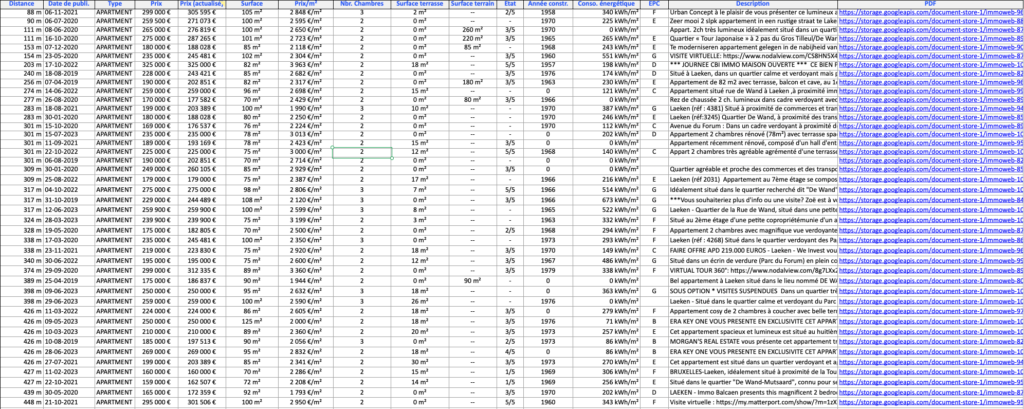

Here is a comparables table obtained thanks to the Market Explorer application:

It is then very useful to calculate the price/m2, the average price or to create a price histogram. This will allow you to complete your analysis with the minimum, median, and maximum price of the sample.

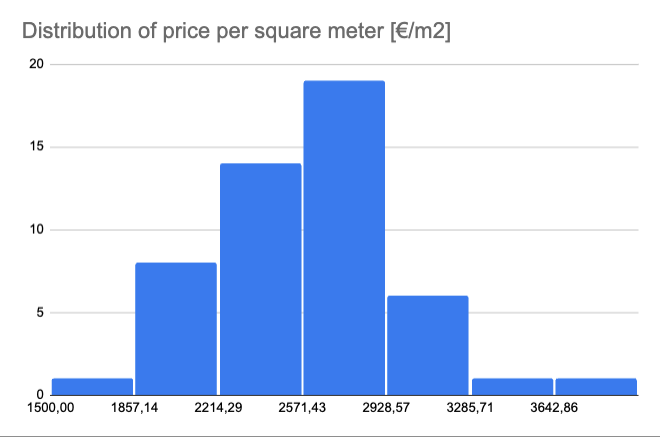

Thanks to the histogram, we see that 19 properties are in the range €2,570/m2 to €2,928/m2. On the other hand, there is only one property below €1,857/m2 and one property above €3,642/m2. For this sample, the median price is €2,597/m2.

Comparison of methods

Even though these methods are complementary, some of them should be preferred in specific contexts. This is what we will see below:

| Method | Use case | Required data | Advantages | Disadvantages |

|---|---|---|---|---|

| Replacement value | Insurance | – Construction price (€/m2) – Gross area (m2) – Level of depreciation | ✅ Easy to calculate ✅ Requires little information | ❌ Simplistic approach ❌ Sometimes quite far from market values ❌ High sensitivity of the result to the chosen depreciation coefficient |

| Capitalization value | Investment property: income-producing building, student housing, office building or retail. | – Actual or estimated rent – Capitalization rate | ✅ Makes it possible to put yourself in the investor’s position, with a yield in mind – Often makes it possible to obtain more than with other methods if the building is profitable | ❌ Sometimes gives “off-market” values if the building is very profitable (e.g., AirBNB rental) |

| Comparison value | Property not intended for yield | – Comparables | ✅ Method that takes into account the real state of the market | ❌ Need to obtain comparables, sometimes difficult to find |

It is often very useful and instructive to compare the values obtained by the different methods, notably in the case of a change of use (office to residential, traditional housing to student housing).

Example

Let’s take the case of a 200 m² house on a 1,000 m² plot on the outskirts of Nivelles (Walloon Brabant).

| Method | Calculation | Value obtained |

|---|---|---|

| Valuation by replacement cost | – Land: €170,000 (€170/m2) – Construction: €360,000 (€1,800/m2) – Depreciation: 25% – Replacement value: €424,000 | 424.000€ |

| Valuation by capitalization | – Rent: €1,280/month (€6.4/m2) – Capitalization rate: 3.4% | 384.000€ |

| Valuation by comparison | – Median specific price: €2,088/m2 – Total price : €417,600 | 417.600 |

It is interesting to note the following elements:

- for an investor, the expected yield will probably be at least 4% gross. To invest in the property, taking into account the rent and the expected yield, the investor will therefore not want to pay more than €384,000 (i.e., 8% less than the comparison value).

- the replacement value is quite sensitive to the chosen depreciation coefficient. By varying it by 5% down and up, we obtain a range from €397,000 to €450,500.

- for an income-producing building, you can calculate the capitalization value (since it is an investment property) and divide the value by the area to obtain the price/m2. You can then compare this price/m2 to the one obtained by comparison.

Conclusions

We have seen three valuation methods:

- Valuation by replacement cost

- Valuation by income capitalization

- Valuation by comparison

Each of these methods can be used in a specific context, but it is always interesting to use them together and compare their results.

Do you need data for your estimates? Our application Market Explorer has a substantial history across several market segments and throughout Belgium. Contact us to find out more!